Every one of these myths serves someone else's interest — not yours. Let's eliminate them one by one.

Myth 1: "VA Loans Are Harder to Close"

False. This myth originated with sellers and listing agents who had one bad experience with an unprepared VA buyer years ago. With an experienced VA lender and a knowledgeable agent, VA loans close on par with conventional loans. What's actually true: VA loans have a required appraisal with minimum property requirements — which protects the buyer, not slows the deal.

Myth 2: "You Can Only Use Your VA Loan Once"

Completely false. VA entitlement is restorable and in many cases partially available for simultaneous use. The VA loan is designed to be a reusable lifetime benefit — not a one-time coupon. Service members have used their VA loan three and four times.

Myth 3: "VA Loans Are Only for Single-Family Homes"

Wrong. The VA loan covers 1–4 unit residential properties. Duplexes, triplexes, and fourplexes are all VA-eligible — as long as you occupy one unit as your primary residence. This is the foundation of the house hacking strategy.

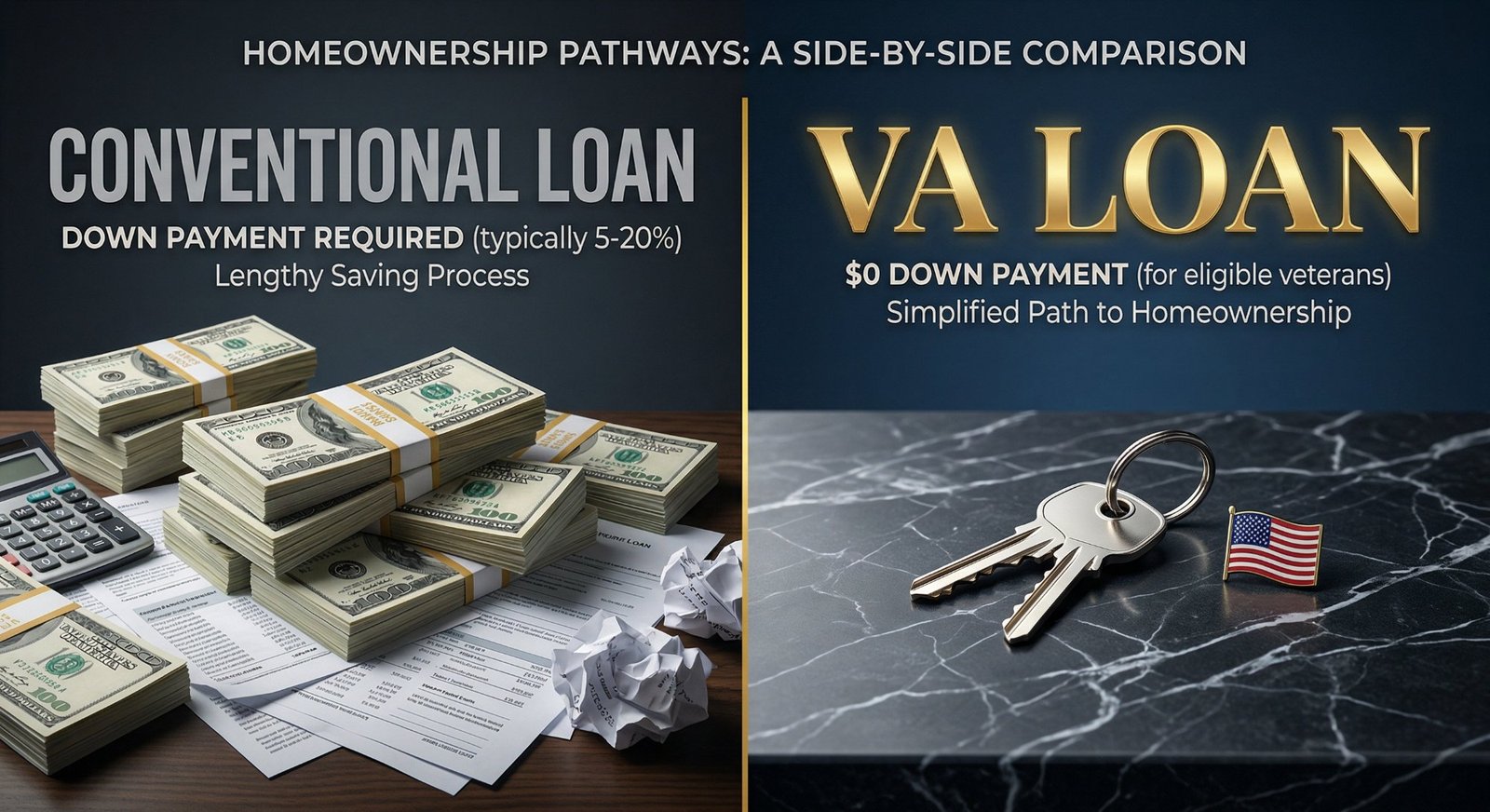

Myth 4: "I Need Perfect Credit"

Not true. The VA doesn't set a minimum credit score — lenders do. Most VA lenders approve at 620+. Some work with scores as low as 580. The VA guarantee reduces lender risk, which is why they're often more flexible on credit than conventional loan programs.

Myth 5: "VA Loans Have Higher Interest Rates"

Generally false. VA loans typically carry rates at or below conventional loan rates — because the government guarantee reduces lender risk. Shop multiple lenders. VA mortgage rates are competitive, often the most competitive available to any buyer.

In 2024–2025, VA loan rates have consistently run 0.25%–0.5% BELOW comparable conventional loan rates for qualified buyers. On a $600,000 loan, that's $900–$1,800/year in savings — every year for 30 years.

Myth 6: "VA Loan Offers Don't Compete in Hot Markets"

Outdated and largely incorrect. An experienced VA agent knows how to write competitive offers. In San Diego's military market, sellers regularly accept VA offers. The key is working with an agent who knows how to make VA offers strong — not one who apologizes for the loan product.

Myth 7: "The VA Funding Fee Makes It Not Worth It"

False. The VA funding fee (typically 1.25%–3.3% of loan amount, depending on service category and down payment) is the one real cost of VA vs. conventional. But it can be rolled into the loan (zero out-of-pocket), and it's dramatically cheaper than years of PMI plus a 5–20% down payment. The math is not close — VA wins almost every time.

| Cost Factor | VA Loan ($600K) | Conventional (5% down) |

|---|---|---|

| Down payment | $0 | $30,000 |

| PMI (monthly, ~5 yrs) | $0 | ~$11,700 total |

| Funding fee | ~$15,000 (rolled in) | $0 |

| 5-year net cost difference | VA saves ~$26,700 in cash out-of-pocket | |

Book a free 30-minute strategy call with Mike Barajas. He'll review your rank, your BAH, and your goals — and build a real plan. DRE #2511286 · (619) 567-5988

Book a Free Strategy Call